Update on Korea

Dalton Investments (“Dalton”) continues to believe that there is a compelling long-term opportunity for investors in Korea, due to the country’s very low valuations and improving corporate governance and capital allocation practices. As an engaged investor, Dalton believes that it has the ability (alongside other local and international activists) to drive change and unlock the long standing “Korea discount.”

Record Local Retail Stock Purchases

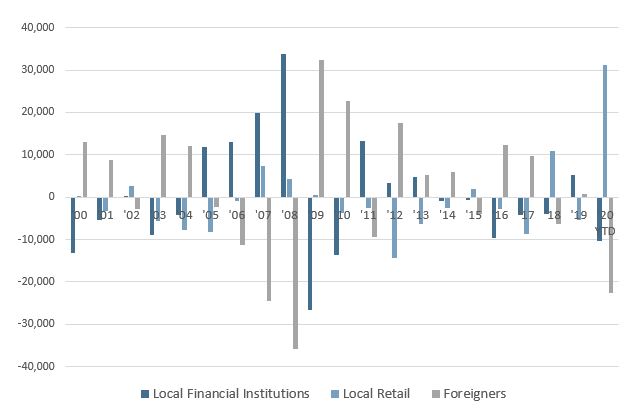

Since the Global Financial Crisis, Korean retail investors have been limited participants in the domestic market, preferring to invest in real estate or hold cash. However, this trend has reversed strongly this year, with approximately KRW 31 trillion (USD 21 billion) in net purchases by retail investors so far in 2020. As the chart below shows, the net purchase here represents by far the largest one in the last twenty years.

Korean Stock Market Money Flows (KRW Bn)

Source: Korea Exchange

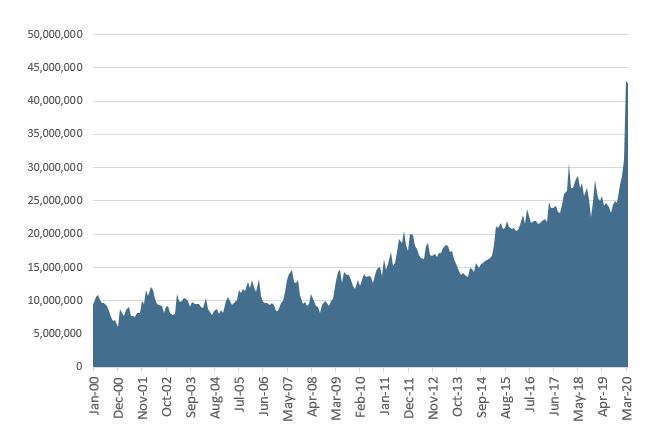

Interestingly, these purchases began in earnest after the COVID-19 pandemic began to negatively impact the Korean equity market. Local investors appeared to view the sell-off as an opportunity to invest in businesses like Samsung Electronics, with the belief that these high-quality franchises will be able to survive the global economic fallout from the pandemic. These purchases have generally been made directly by retail investors, rather than through pooled funds, due to a general distrust of the local Korean mutual fund industry. Local retail investors’ deposits in brokerage accounts also have increased significantly as seen below.

Korean Retail Investor Deposits (KRW mn)

Source: Korea Financial Investment Association

One explanation for this change in behavior can be found in the strong appreciation of the Korean real estate market over the past 10 years and the determination of the Korean government to contain further price rises in real estate. Dalton believes that many highly affluent investors, who have made significant profits in the real estate market, have now begun to invest these profits in the stock market. However, this buying is not limited to the wealthy; a general view appears to be forming among the general public that stocks are one of the few ways for ordinary people to build wealth. This change in mindset is particularly apparent in young Koreans. Personal wealth and business-related YouTube content has been flourishing in Korea, with a single helpful video from a Korean “money management expert” gaining 1.5 million views in just a few months. The video highlighted the powerful effect of saving money by avoiding wasteful expenses and accumulating stocks for the long term.

Although this clear shift in behavior is encouraging, we note that it represents just the tip of the iceberg, with Koreans currently sitting on around USD 1 trillion in cash and deposits, and a mere 2% of retirement pensions invested in stock market investments.[1]

The Ruling Party Solidifies Its Power

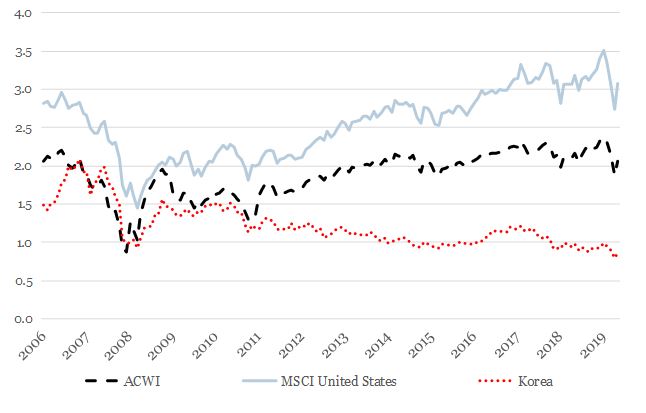

Korea held a general election in April, with the ruling Democratic Party and its satellite, the Platform Party, winning a landslide victory, taking 180 of the 300 seats of the Parliament (60%). Dalton believes that this victory likely will expedite the current government’s push for economic democratization. The government previously has proposed changing commercial law so that minority shareholders can protect and exercise their rights more aggressively, preventing further unfair treatment from controlling shareholders. Previously, many of these initiatives were hindered by the United Future Party opposing the current administration, which used to hold a larger number of seats prior to the April 2020 election. We believe that enacting measures to better protect minority shareholders would be tremendously helpful in improving the perceived poor corporate governance of Korean companies a key reason for the continued “Korean discount” in the Korean stock market (see below).

Price/Book

Source: MSCI

Samsung Electronics’ JY Lee Apologizes

Vice Chairman of Samsung Electronics, JY Lee, made a public apology on May 6, regarding the company’s role in a corruption scandal that resulted in the impeachment of former president Park Geun-hye. Lee also vowed not to hand the management of the company to his children. Family succession of management control previously practiced by the Lee family has been seen as the root cause of the company’s historic poor corporate governance, including unfair mergers, “tunneling” of company assets (where majority shareholders direct company assets to themselves for personal gain) and the general abuse of minority shareholder rights.

The motivation for this public apology appears to be Lee’s upcoming re-trial related to the corruption scandal and his desire to avoid a second spell in prison. Whether Lee will deliver on his promise after the conclusion of the trial is uncertain, but Dalton believes that Korea’s largest Chaebol publicly admitting guilt may boost people’s views on the improvement in Korea’s corporate governance.

Increasing Buybacks, Gifts and Stock Compensation

As the Korean stock market was declining sharply in February and March in reaction to the COVID-19 outbreak, there was a significant increase in the number of share buyback announcements from companies. Through the end of April, the number of buyback announcements was around 500, six times greater than the number during the same period last year. The total value of the buyback also increased approximately five times compared to the same period last year. Given the very low valuation of the Korean market and the overcapitalized nature of many Korean companies (with excess cash on balance sheets), Dalton views this action very positively and believes it should add material long-term value for shareholders. Interestingly, a number of majority shareholders also chose this period to gift stocks to their children, implying they viewed the stock price as cheap (making this a good time to gift from a tax perspective). Dalton also has observed an increasing rate of stock option issuance as part of executive and employee compensation.[2] We view this positively in terms of improving alignments of interest with minority shareholders.

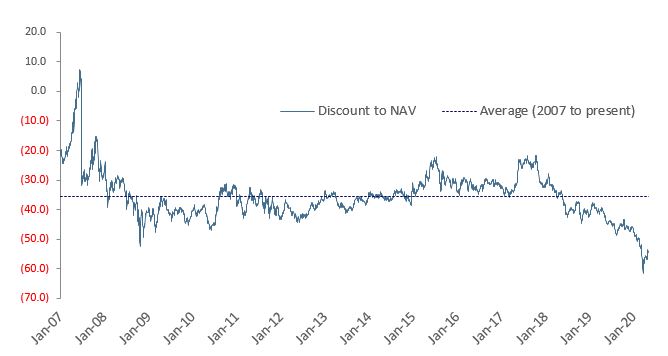

Conglomerate (Holding company) Discount Widening to Extreme Levels

As an investor focused on alignment of interests, a key area of interest for Dalton are Korean holding companies, as these are the entities where the controlling families have concentrated their wealth. Due to this wealth concentration, Korean holding companies have historically been given preferential treatment by the controlling families over their listed subsidiaries. There have also been increasing cases of the families owning high quality private companies at the holding company level, meaning that these holding companies can no longer simply be viewed as an aggregation of listed companies that investors can access separately. Dalton believes alignment of interests has actually been improving in these holding companies, as there has been an increasingly large amount of stock options issued by the holding companies to their key executives. One of the largest holding companies, SK Group, has clearly signaled that future performance bonuses for its executives will be paid mostly through stock options.

A historic criticism of holding companies has been their poor capital allocation, but Dalton has observed a change in behavior here. For example, LG Corp used this market decline to increase its stake in its listed telecom subsidiary LG U Plus. Also, there has been an increase in share buybacks and dividend payments. Despite these positive characteristics and recent improvements, Korean holding companies have grown increasingly out of favor, with their discount to net asset value (NAV) widening to one of its largest levels ever (now greater that the discount reached during the Global Financial Crisis). If in fact Korean companies are practicing better corporate governance, Korean holding companies represent particularly attractive investment opportunities.

Korean Holding Companies Discount to NAV (%)

Source: CLSA

Dalton’s Activism with Sam Yung Trading

Sam Yung Trading is a Korean trading company, which has a valuable joint venture with Essilor Luxottica, the global leader in the eyeglass lens, frames and retail market. The joint venture generates approximately 35% return on capital. Despite this high-quality business, the company’s practice of hoarding cash has caused the company’s enterprise value to be negative (i.e., net cash is larger than the company’s market capitalization). In an effort to change the company’s behavior, Dalton, on behalf of its accounts, made a shareholder proposal recommending two candidates for internal statutory auditor positions on the company’s board. The aim was to place third parties inside the company and to understand the reason for such ineffective capital allocation. Unfortunately, Dalton lost the resulting proxy fight by 5%, due to a local asset management firm who owned a 10% stake siding with the company. Despite this loss, there were small victories to be enjoyed: prior to the company’s annual general meeting, Sam Yung Trading announced a mid-term shareholder return plan, which signaled an increase in dividend by 43% in 2021 and an additional 10% for the subsequent two years. Despite the mixed outcome with Sam Yung Trading, Dalton continues to believe that engagement from activists has the potential to drive material change in Korea.

COVID-19

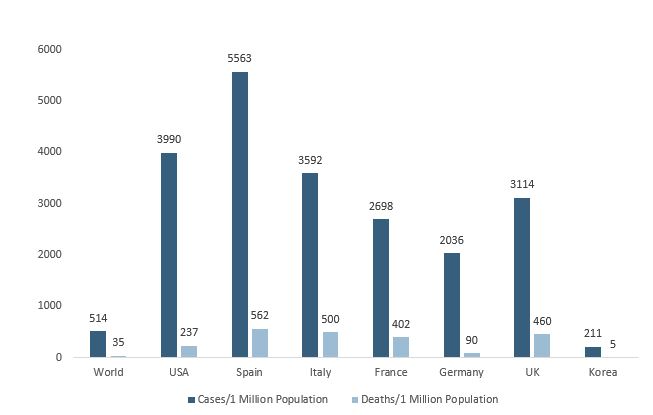

Despite major outbreaks in certain regions (e.g., Daegu), Korea has so far managed to contain the spread of COVID-19 due to widespread use of masks, massive testing programs and generally high levels of transparency. As the chart below shows, the country compares very favorably in terms of the number of cases and deaths versus major western economies. While another wave of the outbreak may happen, Dalton believes that Korea’s handling of the crisis and its ability to quickly manufacture and distribute testing kits have been positive for the country’s global brand.

COVID-19 Cases and Deaths/1 Million Population

Source: https://www.worldometers.info/coronavirus/; 5/8/20

[1] Bank of Korea, Korea Financial Investment Association

[2] Examples include:

- The Chairman of CJ Corp (the 13th largest corporate group in Korea) gifted 1.8 million preferred shares to his son and daughter in April.

- The Chairman of SPC (the number one bakery & café group in Korea) gifted half (4.6%) of his common stock holdings to his son.

- SK Holdings announced 214,000 stock option issuances to its two professional executives, which equate to a base amount of approximately $25 million. Similar types of stock option grants were observed across major SK group companies, such as SK Telecom, SK Hynix and SK Innovation.

- Internet companies Naver and Kakao continued their stock option issuances. Naver issued 680,000 additional stock options to its executives and employees, raising the total stock options issued to 3.0 million. Naver also announced plans to subsidize 10% of employee share purchases in the company (up to KRW 2 million per person). Kakao issued 895,000 additional stock options to its executives and employees, raising the total stock options issued to 2.6 million.